GoDocs wants to point out specifically:

- our documents do not let the borrower wait for insurance or a loan to continue to maintain the property or start fixes.

- The lender has a number of options and they do not have to give the borrower a loan (they can disburse under the current loan if they want).

- The lender has options for what happens next to the insurance proceeds as the borrower has to maintain a policy that puts the lender first.

- borrower fix and get proceeds

- lender fix and uses Indebtedness and insurance proceeds

- Lender calls the loan and exists the relationship - insurance used to pay down the loan or given to borrower at the lender's determination

- any combination of the above or whatever the lender's business decision is.

See more details below that go over these rights ->

Reassurance Regarding Completing Repairs While Waiting for Insurance Proceeds

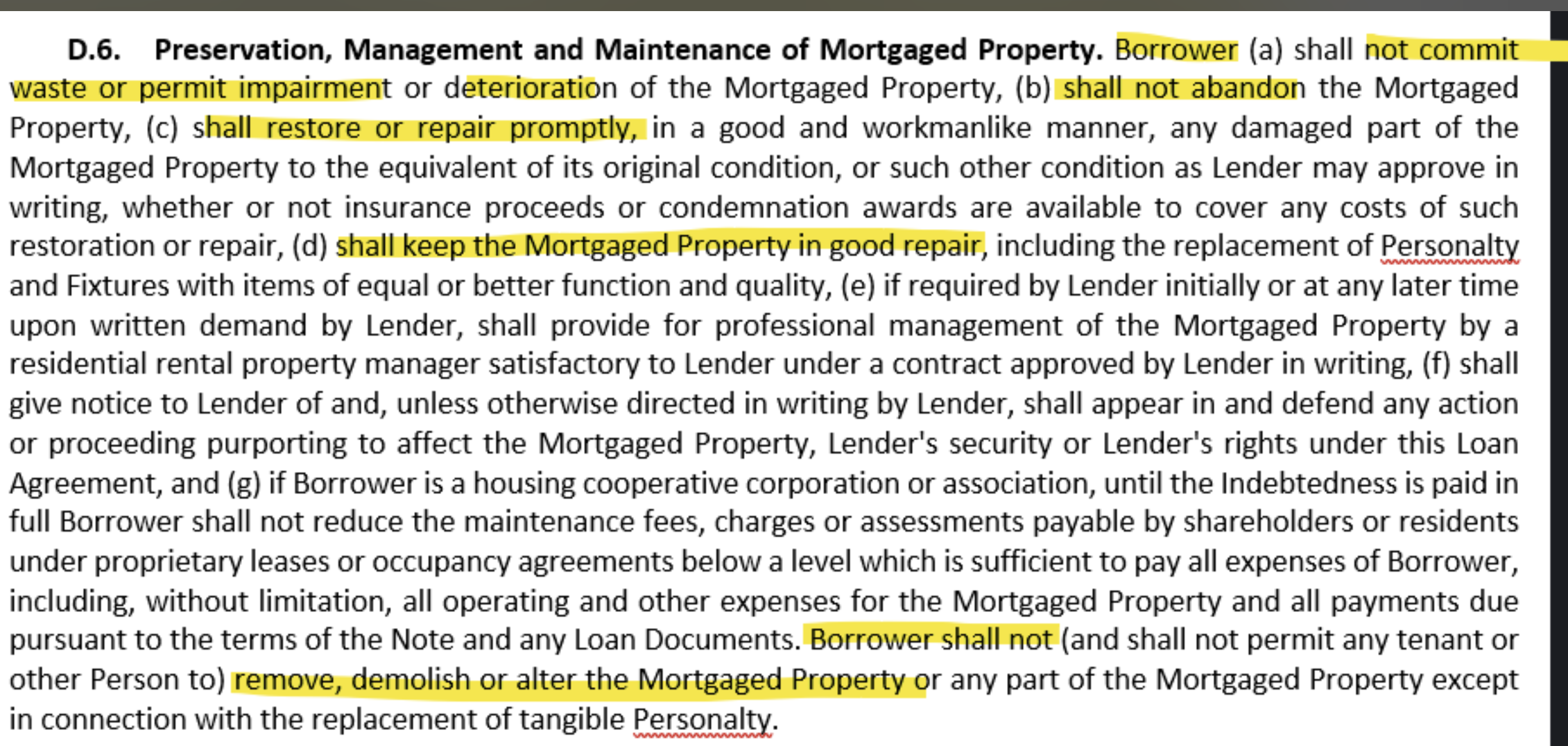

The loan documents make it clear that the property must be maintained and promptly repaired, regardless of whether insurance proceeds are immediately available. Specifically:

- Borrower’s Obligation (Section D.6)

The Borrower is required to restore or repair any damaged part of the property promptly and in a good, workmanlike manner—even if insurance proceeds or condemnation awards have not yet been received. This ensures the property does not deteriorate and remains in good condition.

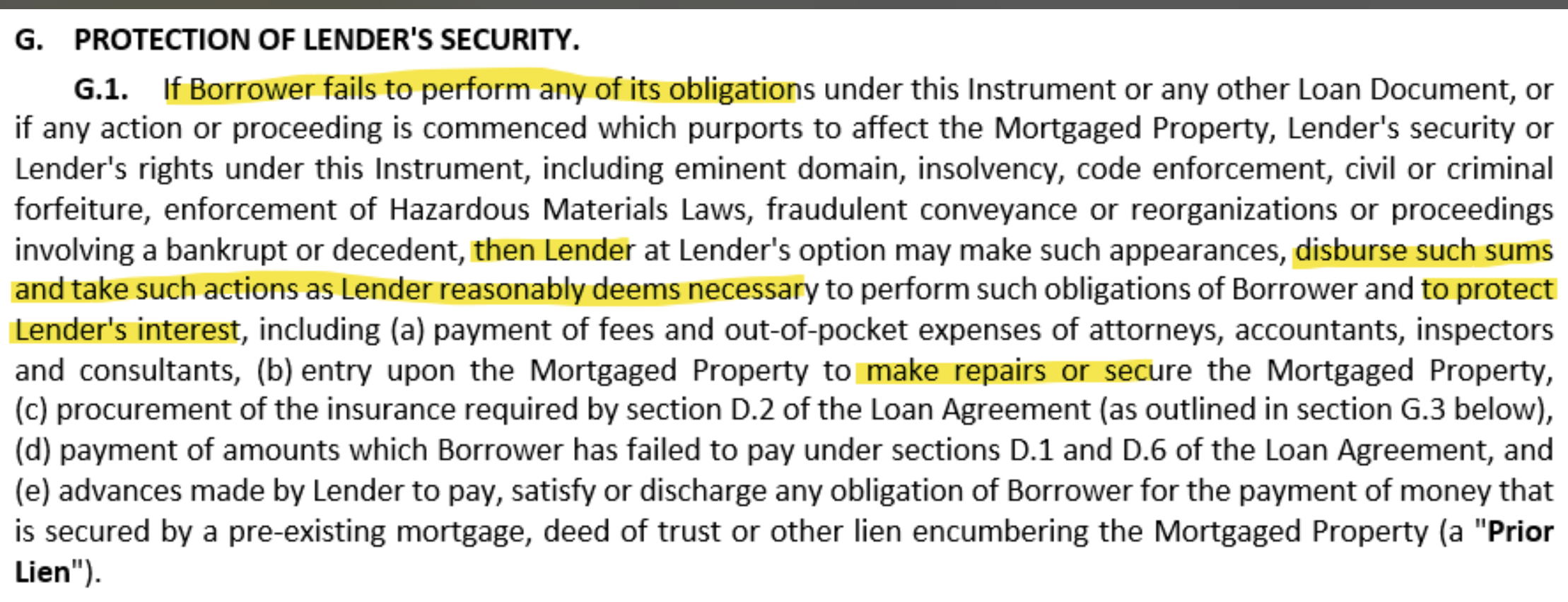

- Lender’s Role (Section G)

If the Borrower is unable to perform these obligations, the lender has the right (but not the obligation) to step in and make repairs or take actions necessary to protect the property and its security interest. Any amounts advanced by the lender for this purpose would be added to the loan balance.

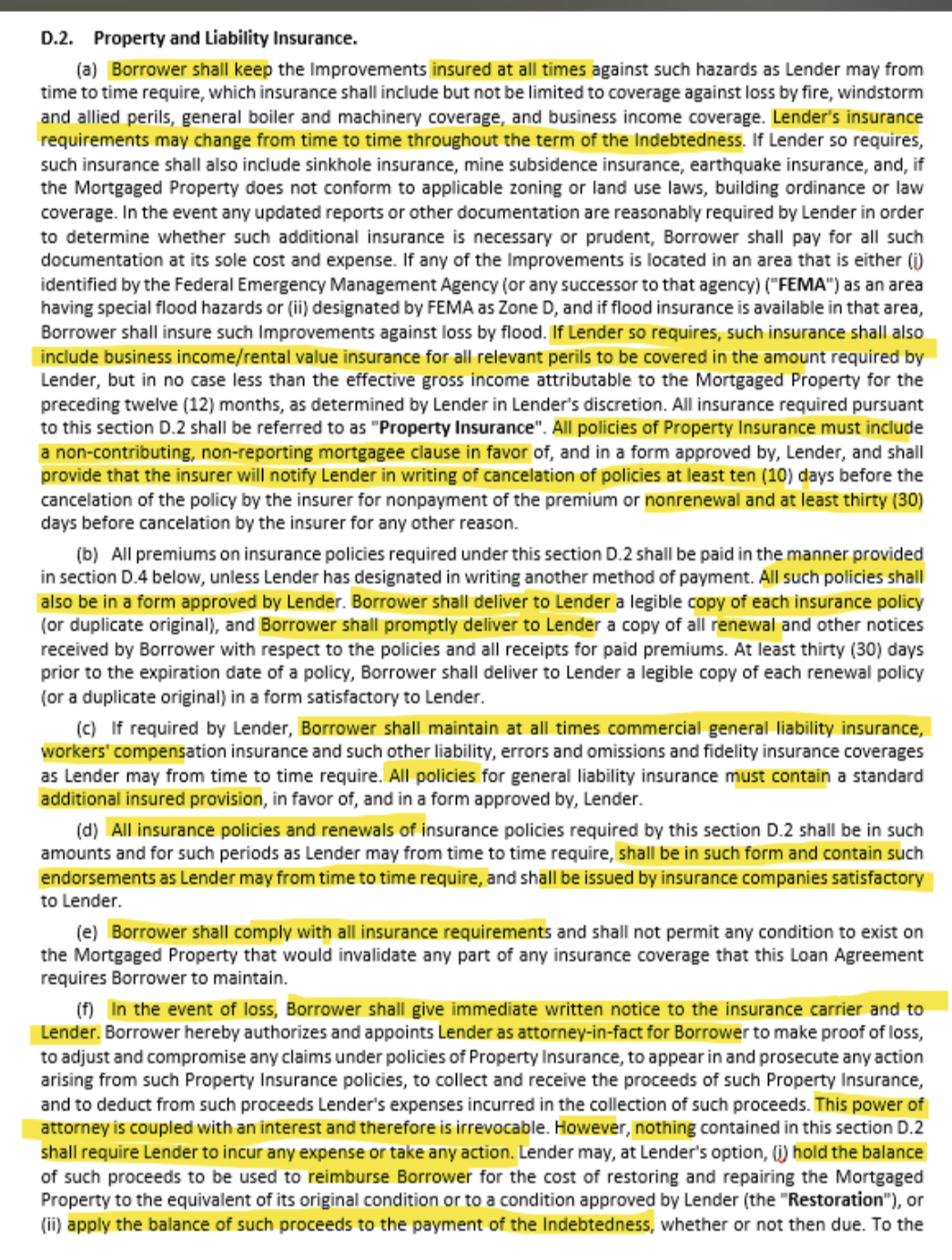

- Insurance Proceeds (Section D.2)

Once insurance proceeds are available, the lender will either:- Hold them for reimbursement of restoration costs, or

- Apply them to the loan balance if restoration is not feasible under the conditions outlined earlier.

- Restoration is the preferred outcome when conditions are met.

What This Means for You

The documents allow insurance proceeds to be used for restoring the property to its pre-claim condition (or a condition approved by the lender). In fact, restoration is the preferred use if certain conditions are met, such as no default, sufficient funds to complete repairs, and lender’s determination that restoration is feasible and timely. If these conditions are satisfied, the lender will not apply proceeds to the loan balance and will instead make them available for restoration.

- The Borrower should begin repairs promptly to comply with the loan agreement and prevent further damage.

- Insurance proceeds will typically be applied toward reimbursing the Borrower for restoration costs if the lender determines restoration is feasible.

- If the Borrower faces challenges funding repairs upfront, communicate with the lender—the lender may advance funds to protect the property, which would later be added to the Borrower's loan balance.

Further, as outline in F.1(b) of the Loan Agreement, "any failure by Borrower to maintain the insurance coverage required by section D.2 above or to timely provide any financial information or documents required..." is an Event of Default.

During an Event of Default, the Lender has all remedies available to them, up to and including accelerating the loan.