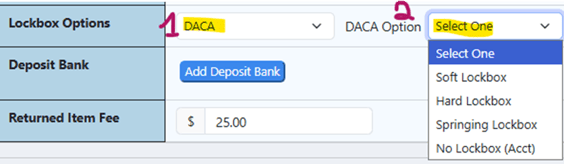

GoDocs offers the below options for Lockbox selections:

- No Lockbox

- Lockbox language only version

- DACA

- Soft

- Hard

- no disbursements

- discretionary disbursements

- Springing

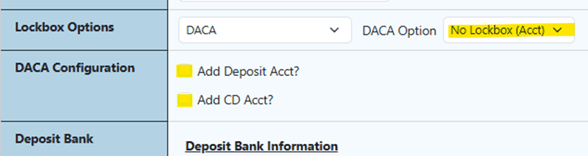

- No Lockbox (Acct)

- Add Deposit Acct?

- Add CD Acct?

Compare of No Lockbox vs Lockbox Language Only

![]()

![]()

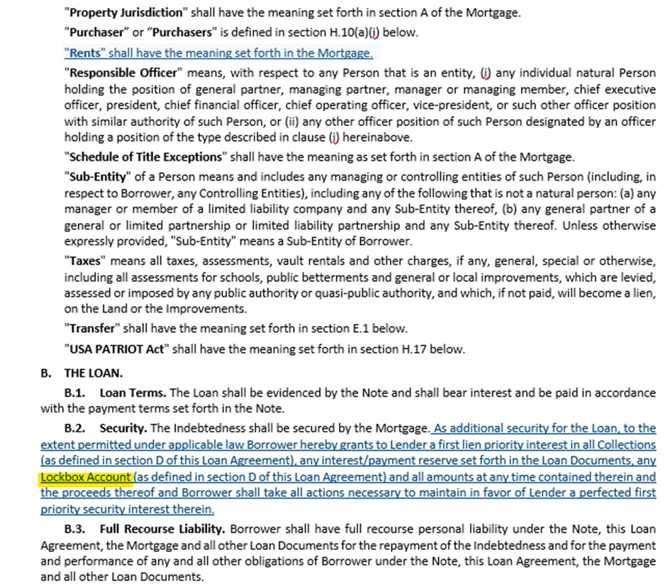

The loan is mainly secured by a mortgage on the property but also giving the lender rights to:

- All money collected from the property (like rent payments)

- Any reserve accounts set aside for interest or payments

- Any lockbox account (a special bank account where income goes)

- All money sitting in those accounts

- Any proceeds that come from those funds

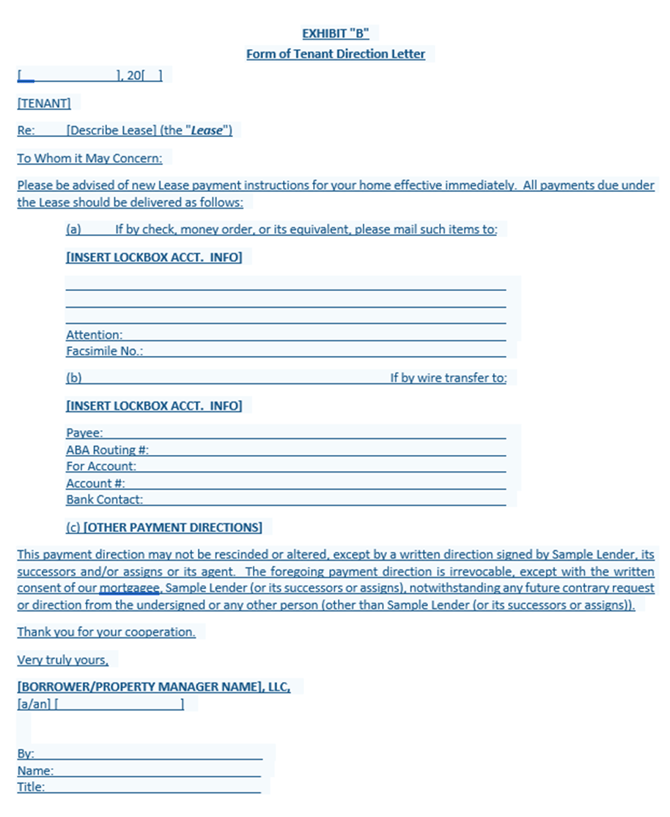

In the Loan Agreement:

The tenant direction letter means that instead of paying the landlord directly, the tenant must send payments to a specific lockbox account (usually controlled by the lender).

In the Security Instrument:

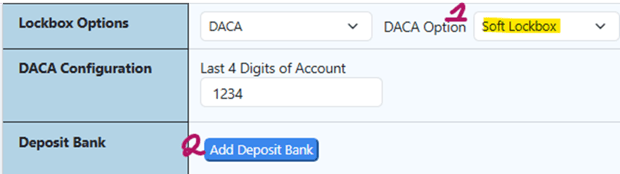

For DACA Lockbox Options:

After selecting DACA, you have four DACA options to choose from in the drop down:

If DACA with Soft Lockbox

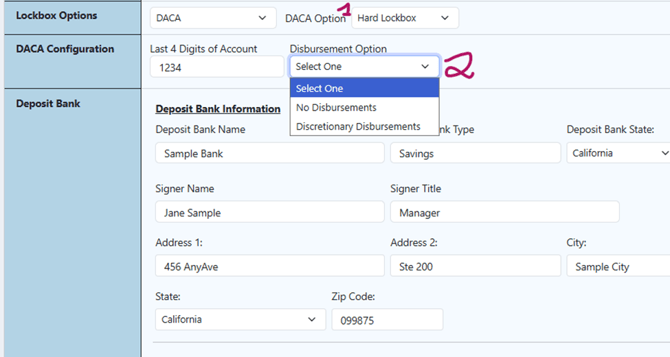

If DACA w/Hard lockbox make a selection for the disbursement option:

For the above Hard Lockbox option you must select from two disbursement options: "No Disbursements" or "Discretionary Disbursements".

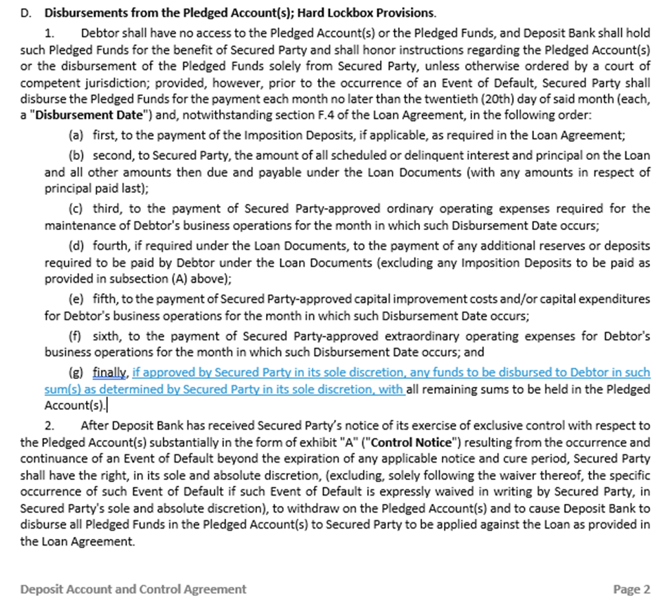

DACA with Hard lockbox with NO disbursements:

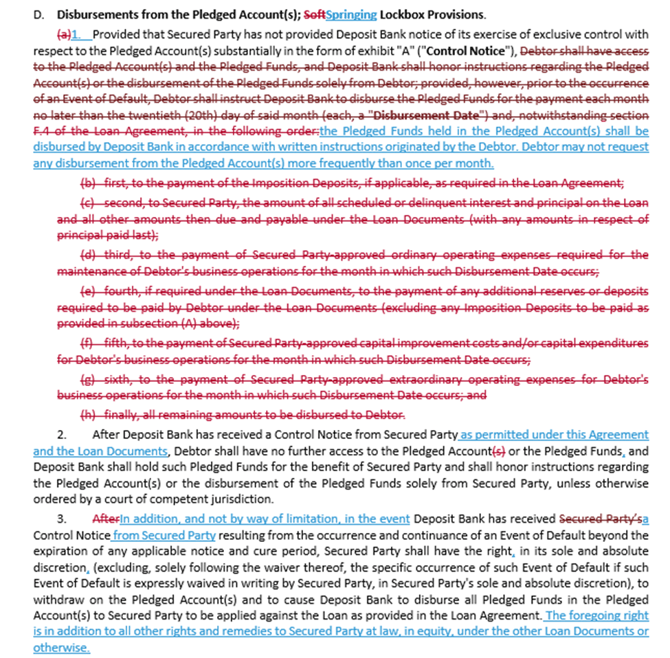

DACA with Hard lockbox with Discretionary Disbursements

Compare of DACA Hard Lockbox vs DACA Soft Lockbox

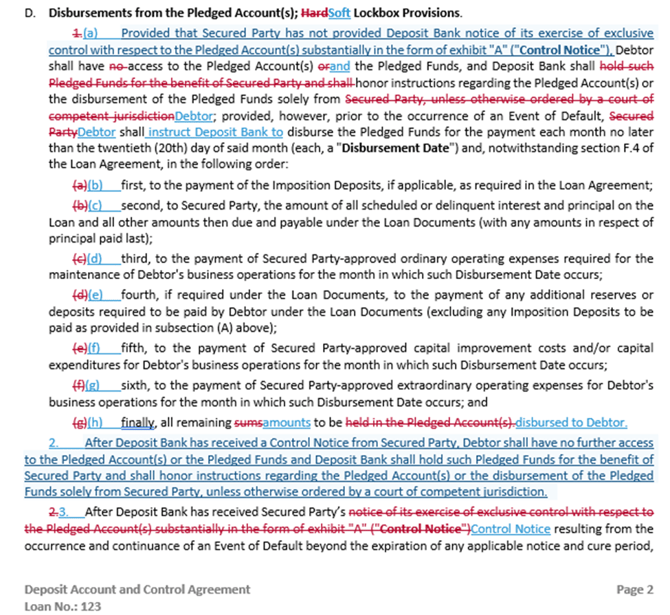

Hard Lockbox = Lender Control ImmediatelyIn the hard lockbox structure, once the lender gives a Notice of Control, the borrower loses access to the account.

The loan documents state that after notice the “Debtor shall have no further access to the Pledged Account(s)… Deposit Bank shall… honor instructions… solely from Secured Party.”

Soft Lockbox = Borrower Control Until Default unless and until a default occurs.In a soft lockbox structure (by contrast), the borrower typically:

- Collects rent into the lockbox account,

- Has access to the funds,

- Can use the money in the ordinary course of business,

Differences In the Deposit Account and Control Agreement:

Compare of DACA Hard - No Disbursements versus

DACA Hard - Discretionary Disbursements

In both versions:

- All rent and revenue goes into a blocked account.

- The lender has sole control of that account

- The borrower has no direct access to the funds

Hard Lockbox – No Disbursements, means that the lender collects the rent and keeps it.

Hard Lockbox – Discretionary Disbursements, is still a hard lockbox — the lender controls the account — but the agreement lays out a structured waterfall for how money gets released in a set order. The borrower can get operating funds — but only if approved and after the taxes, loan payments, operating expenses, any required reserves, approved capital improvements etc are paid first.

Differences in the Deposit Account and Control Agreement:

DACA w/Springing Lockbox

DACA Soft Lockbox versus DACA Springing Lockbox

Difference in the Deposit Account and Control Agreement:

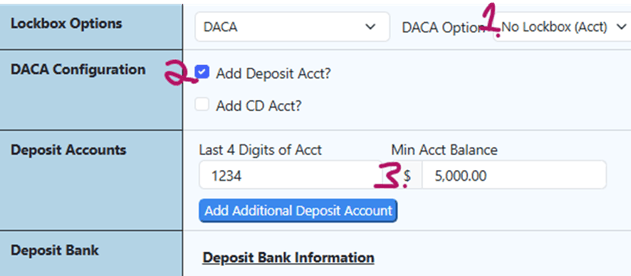

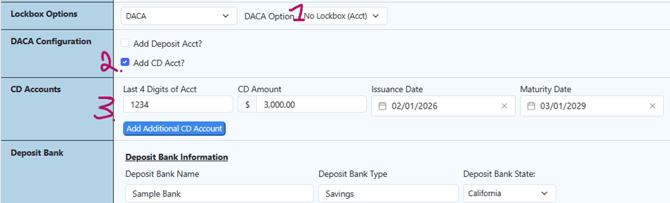

If DACA with NO Lockbox make selection for DACA Configuration:

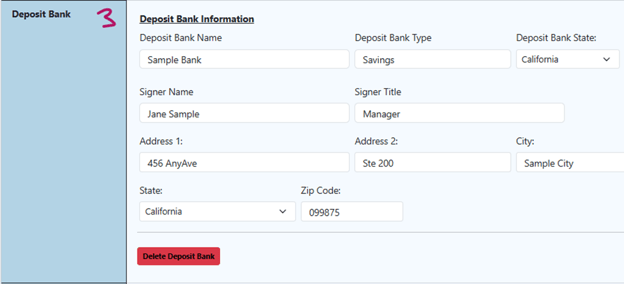

For DACA with No Lockbox you must select to "Add Deposit Account" or "Add CD Account" for the configuration:

If DACA with NO Lockbox with Deposit Acct:

If DACA with No Lockbox – Deposit Account (Standard Bank Account DACA)

This structure involves:

- A regular deposit account (checking or savings)

- A Deposit Account and Control Agreement (DACA) among:

- Borrower

- Lender

- Depository Bank

- Funds flow in and out during normal operations.

- Lender obtains “control” under UCC Article 9.

- Often used for:

- Operating accounts

- Cash collateral accounts

- Reserve accounts

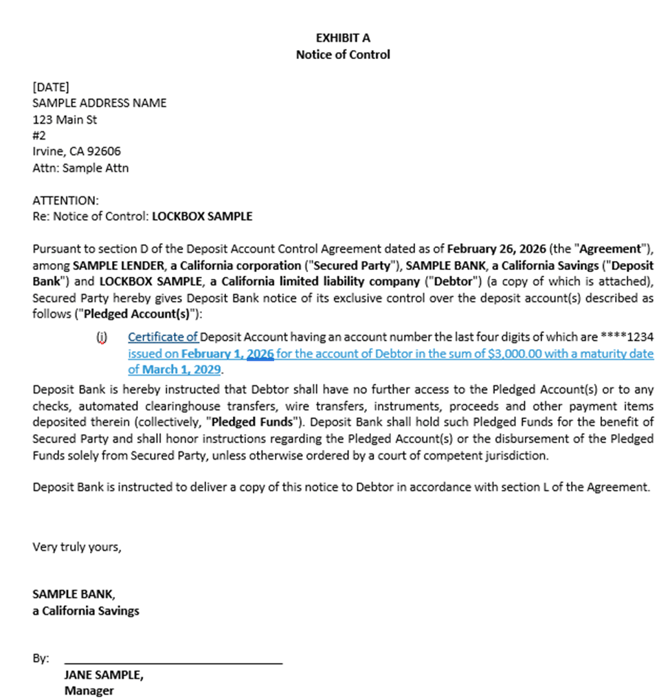

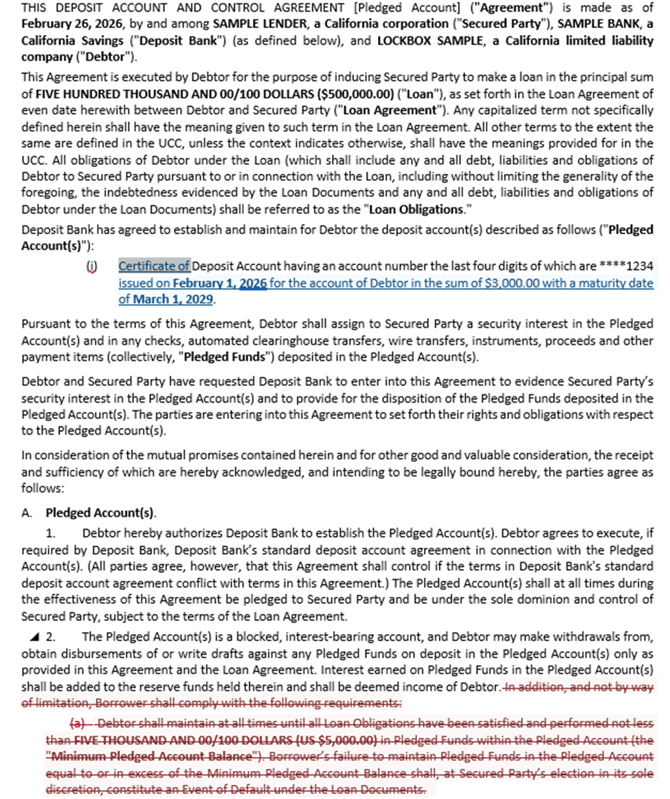

DACA with NO Lockbox with Certificate of Deposit Account:

The No Lockbox – CD Account structure involves:

- A Certificate of Deposit (CD) issued by the bank.

- The CD itself is pledged as collateral.

- A DACA or control agreement provides lender control over the CD.

- Funds are typically:

- Fixed

- Locked for a term

- Interest-bearing

- No operational deposits/withdrawals.

- Often used for:

- Cash collateral securing a loan

- Credit enhancement

- Additional security

Compare of DACA with NO Lockbox with Deposit Acct versus

DACA with NO Lockbox with CD Acct

Use Deposit Account DACA when:

- Borrower needs operational flexibility

- Account will receive rents or revenues

- Funds are moving regularly

Use CD Account DACA when:

- Lender wants clean, static collateral

- It’s purely additional security

- No operational activity is needed

Differences in the Deposit Account and Control Agreement

Differences in the Deposit Account and Control Agreement – Exhibit A: