Difference between no short month interest and a yes 30-day stub interest:

If your selection is set to "YES” Stub interest, one does pay extra interest upfront for the days from Funding date to first payment cycle. That first period is not a full month, so it’s charged separately as “stub interest”. After that then your normal monthly payments begin.

If your selection is set to "NO” stub/short‑month interest, no separate partial‑month interest is charged. Instead, the first payment just covers a full period as the lender basically rolls or skips that partial period.

A stub period = a partial month between when the loan funds and the next scheduled payment date.

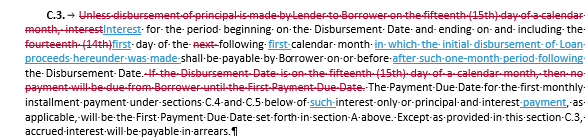

The difference will be in the Note of the loan documents, specifically in Section C. 3 (or thereabouts):

Difference between yes short month interest and a yes 30-day stub interest:

If your selection is set to "YES” stub interest, it is interest for the actual partial period between the loan funding (closing date) and the start of the normal payment cycle (usually the 1st of the next month). It is calculated using the exact number of days in that gap. So the amount can vary depending on how many days there are.

If your selection is set to "YES” 30-Day Stub Interest, it also includes a “stub period” (partial month at the beginning).It is forced to a fixed 30-day period, even if the actual gap isn’t 30 days. Lender is using a standardized 30-day charge (common with 360/30 loan conventions).If the loan closes mid-month, you pay interest for those extra days separately, and after that, normal monthly payments begin.

The difference will be in the Note of the loan documents, specifically in Section C. 3 (or thereabouts):