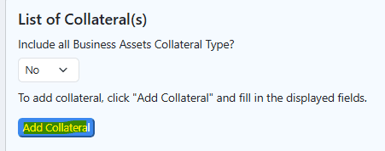

Under the Collateral Tab the customer is able to "Add Collateral":

![]()

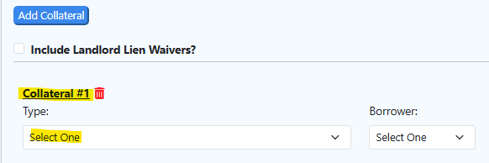

Once the Add Collateral has been clicked the below fields open:

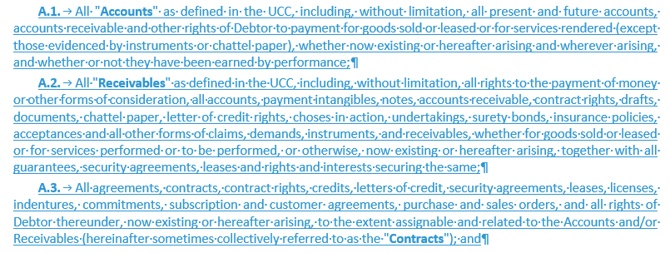

Accounts and Receivables Collateral:

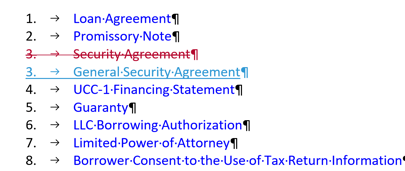

References in the Loan Agreement (Defined Terms, C.4(c), D.9(a)):

![]()

![]()

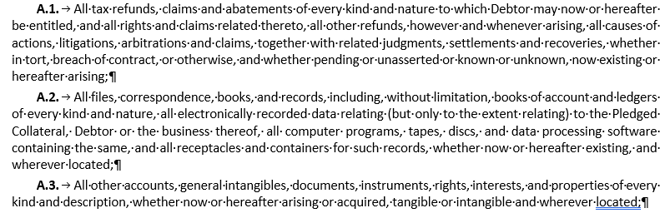

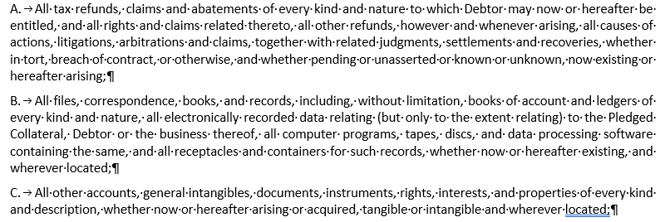

References in the Security Agreement (Section A, C):

References in the Exhibit A of the UCC-1:

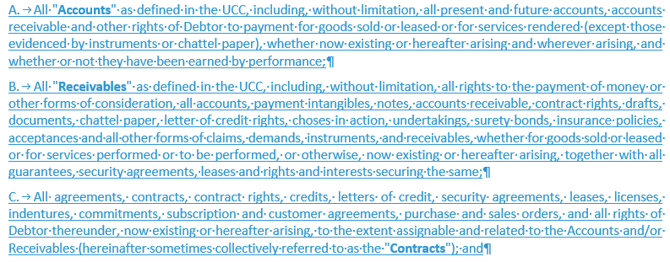

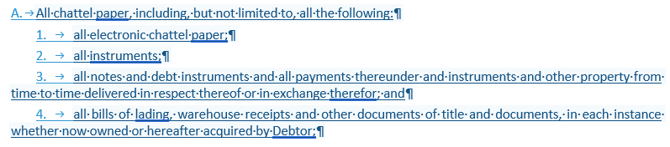

Chattel Paper as Collateral:

The collateral is all financial documents the company owns that represent money owed to them, including Lease contracts, finance agreements, notes owed to them, shipping & storage documents and all money or value that comes from those documents, now or in the future.

References in the Security Agreement (Section A, C):

References in the Exhibit A of the UCC-1:

Contracts as Collateral:

References in the Security Agreement (Section A):

References in the Exhibit A of the UCC-1:

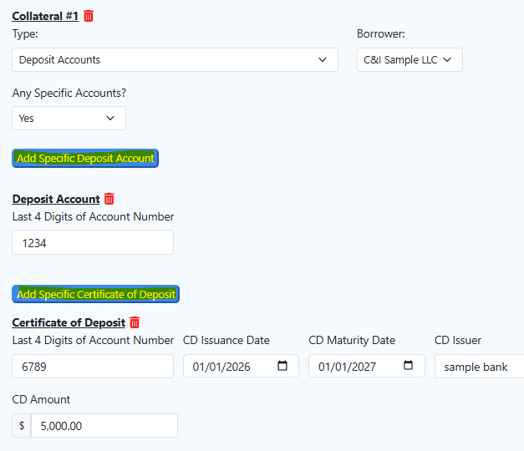

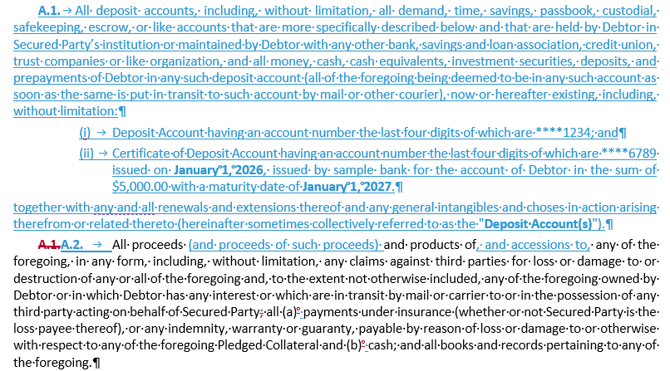

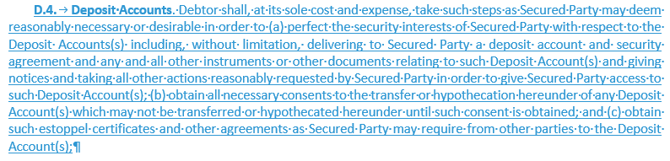

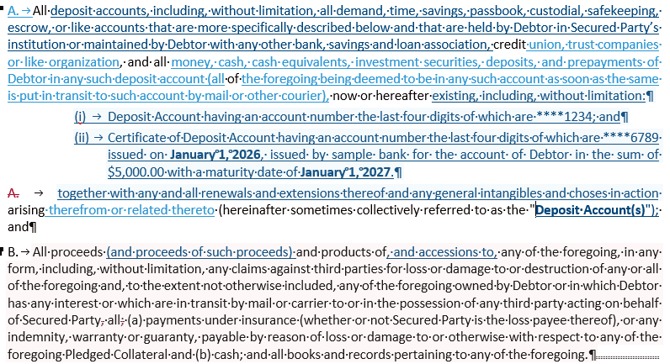

Deposit Accounts as Collateral:

The lender is taking a claim on the Borrower’s bank money, its bank accounts and CD. To secure the loan, Borrower is pledging its cash and bank accounts as collateral. If it looks like company cash or turns into company cash, it’s part of the collateral.

References in the Loan Agreement (Defined Terms):

![]()

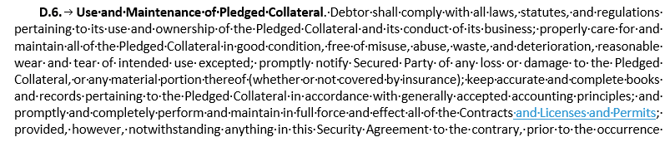

References in the Security Agreement (Section A & D):

References in the Exhibit A of the UCC-1:

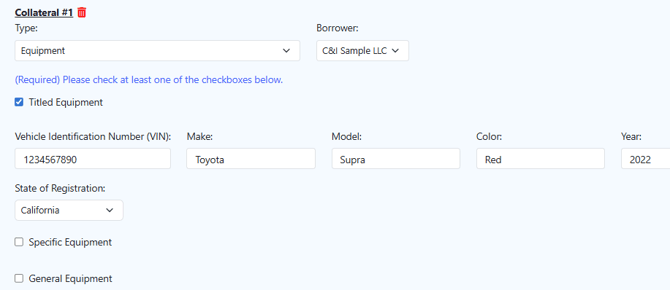

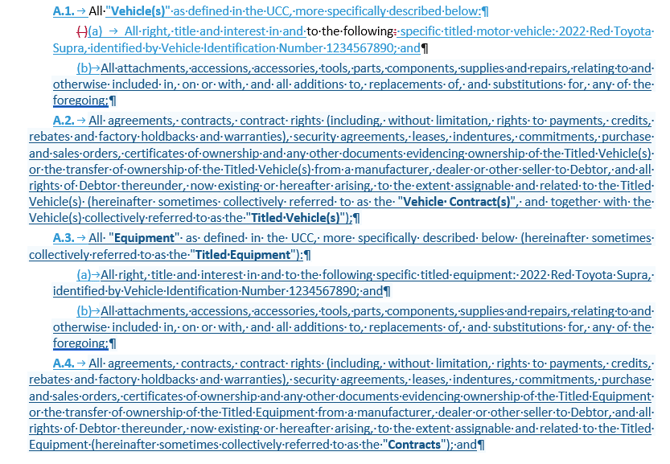

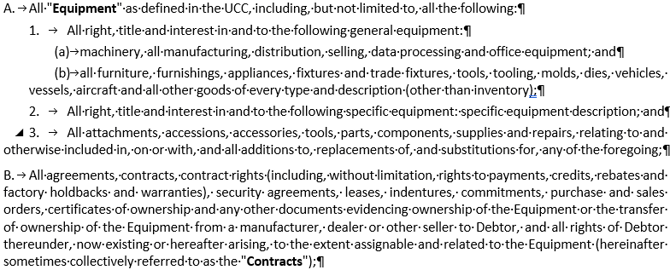

Equipment (titled, specific, general) as Collateral:

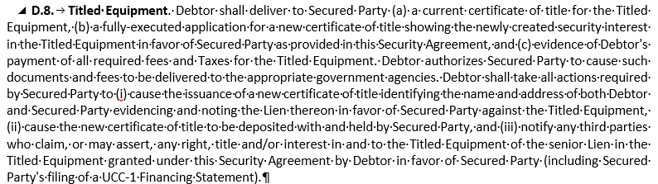

Titled Equipment as Collateral:

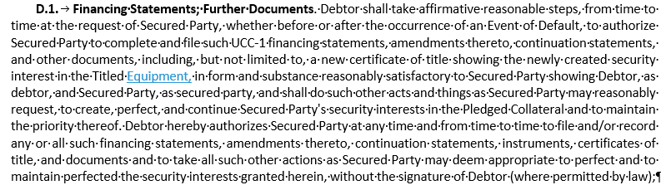

References in the Loan Agreement (Defined Terms, section C.4(c), d.9(x)):

![]()

References in the Security Agreement (Section A & D):

References in the Exhibit A of the UCC-1:

Specific Equipment as Collateral:

References in the Loan Agreement (Defined Terms & D):

![]()

References in the Security Agreement (Section A & D):

References in the Exhibit A of the UCC-1:

General Equipment as Collateral:

Difference between selecting general equipment versus special equipment will relfect in the security agreement:

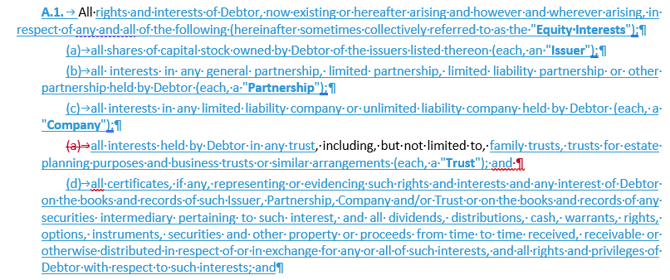

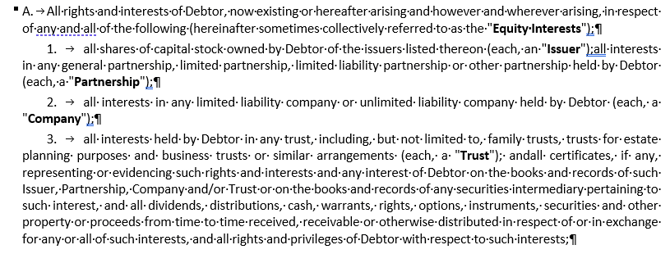

Equity Interest as Collateral:

: ownership interests, money and income tied to those interests, business assets (now and in the future), Insurance and legal proceeds and books and records.That means if the loan isn’t repaid as agreed, the lender has the right to take and sell these items to get repaid.

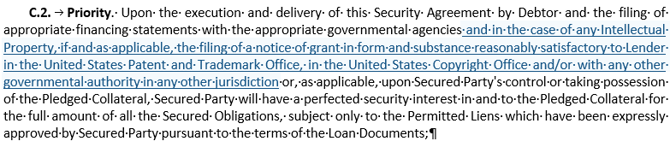

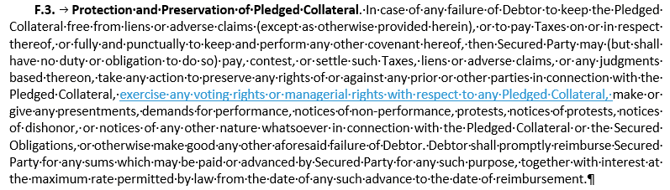

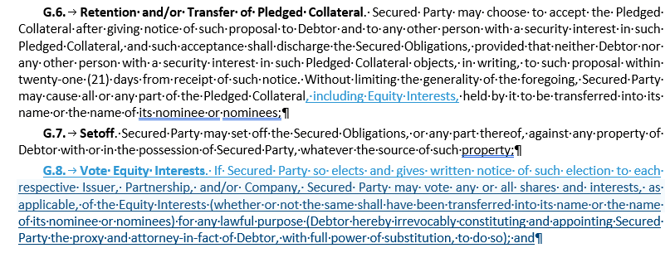

References in the Security Agreement (Section A, F & G):

References in the Exhibit A of the UCC-1:

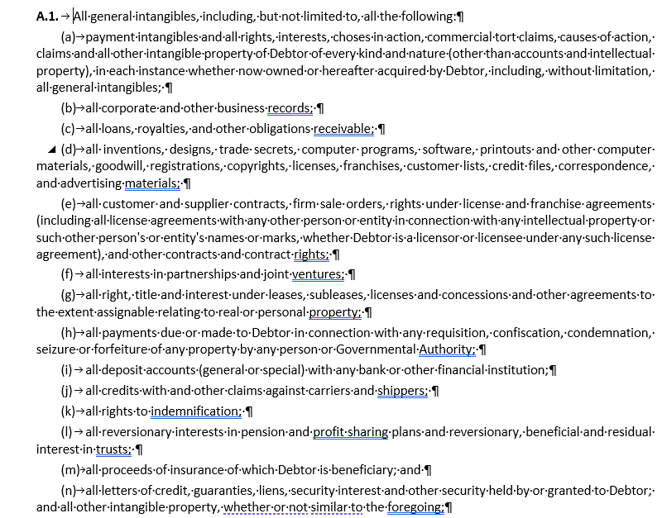

General Intangibles as Collateral:

References in the Security Agreement (Section A & D):

References in the Exhibit A of the UCC-1:

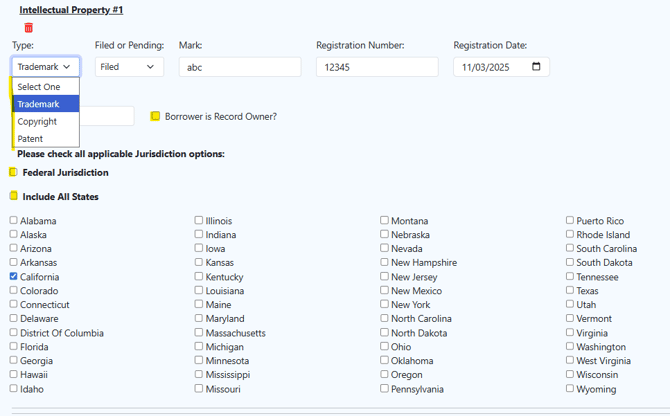

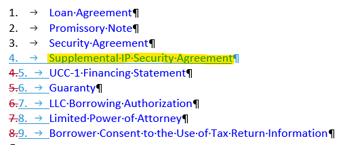

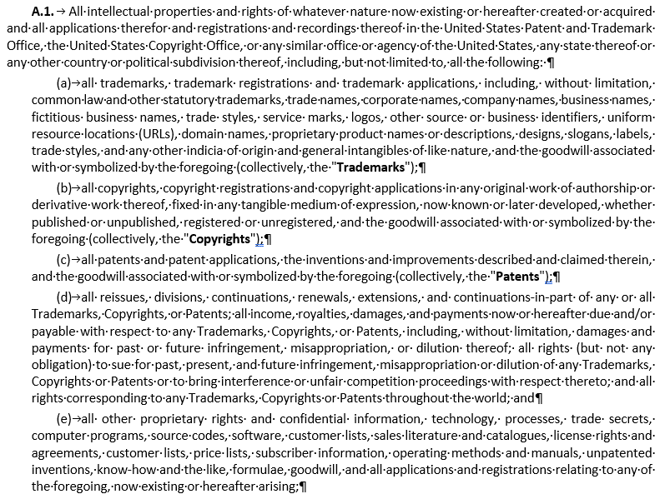

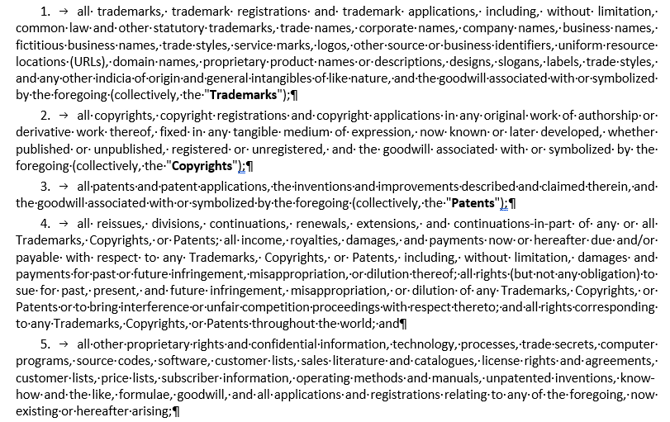

Intellectual Property as Collateral:

References in the Security Agreement (Section A):

Separate Supplemental Intellectual Property Security Agreement see link for sample: Supplemental Intellectual Property Security Agreement

References in the Exhibit A of the UCC-1:

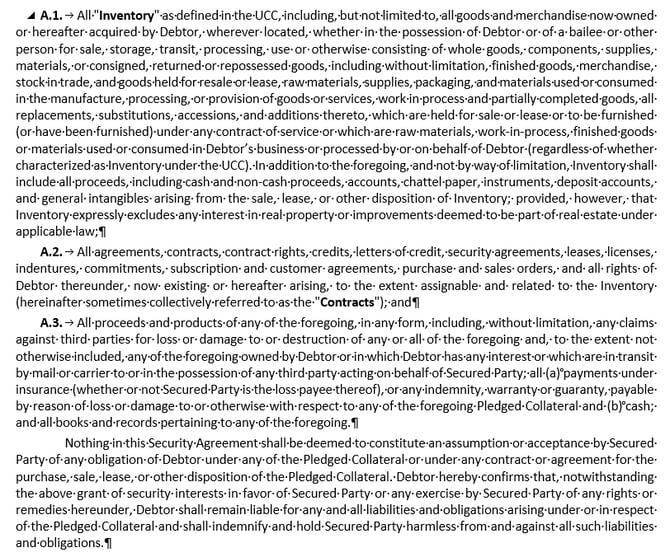

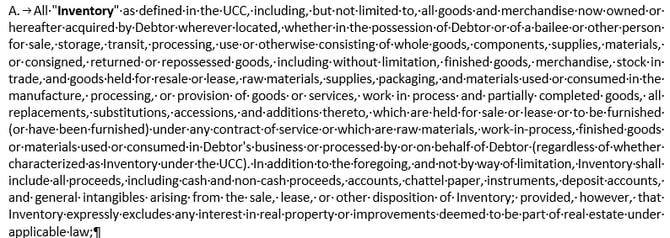

Inventory as Collateral:

References in the Loan Agreement (Defined Terms, Section C.4.(c), D.9.(a)):

![]()

References in the Security Agreement (Section A):

References in the Exhibit A of the UCC-1:

Investment Property as Collateral:

References in the Security Agreement (Section A):

References in the Exhibit A of the UCC-1:

Key Person Life Insurance as Collateral:

Key Person Life Insurance is collateral that is intangible and event-driven (death) and includes much more than just death benefits: the policy itself, the death proceeds, cash surrender value, dividends, claims and contract rights specifically tied to an identified executive (“Key Person”) whose continued involvement is critical to the business.

References in the Loan Agreement (Defined Terms, D.2.(d)):![]()

References in the Security Agreement (Section A & C):

References in the Exhibit A of the UCC-1:

Leasehold Improvements as Collateral:

This is a lender taking a claim on the physical stuff borrower added or built inside a rented space: Walls, partitions, counters, built‑in cabinets and shelving, lighting, plumbing, HVAC, wiring, fixtures, security systems. Basically, it’s the improvements that were paid for to make the space work for the business, even though they don't own the building itself. It’s not cash and not easy to sell, it can lose value quickly, if the lease ends, the landlord may keep it and the lender may need landlord permission to access or remove it.

References in the Loan Agreement (Defined Terms, D.9.(a)):![]()

References in the Security Agreement (Section A & C):

References in the Exhibit A of the UCC-1:

Licenses/Permits as Collateral:

References in the Security Agreement (Section A, D & E):

References in the Exhibit A of the UCC-1:

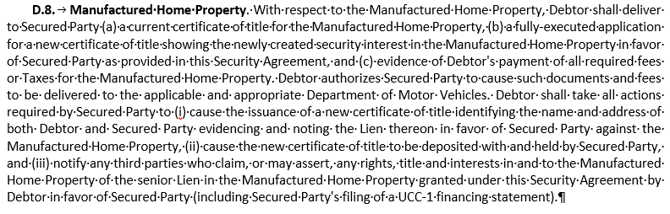

Manufactured Home Property as Collateral:

The collateral is a specific manufactured home and anything tied to it. More specifically, the borrower is pledging: 1) One manufactured home identified by a specific Vehicle Identification Number (VIN); 2) Everything attached to or included with that manufactured home, such as built‑in fixtures or related personal property; 3) Any money connected to that home, including Insurance payouts if it’s damaged or destroyed, Proceeds if it’s sold and claims, warranties, or settlement money. If the loan isn’t repaid, the lender can take and sell the manufactured home (and any related insurance or sale proceeds) to recover the money owed.

References in the Security Agreement (Section A & D):

References in the Exhibit A of the UCC-1:

Marketable Securities as Collateral:

(without a specific account)

(with a specific deposit account)

References in the Security Agreement (Section A & C):

References in the Exhibit A of the UCC-1:

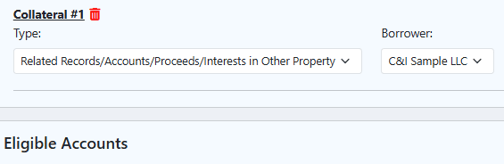

Related Records/Accounts/Proceeds/Interest in Other Property as Collateral:

Basically, the lender has a claim on almost everything the business owns or will own. More specifically, the collateral includes: All business assets, Money the business is owed, Business records and data, Cash and proceeds

References in the Security Agreement (Section A):

References in the Exhibit A of the UCC-1:

Rolling Stock as Collateral:

References in the Loan Agreement (Defined Terms, D.9.(a)):![]()

References in the Security Agreement (Section A, C, D, E & Schedule 1):

See Sample PDF of Memorandum of Security Agreement here: Memo of Security Agreement

References in the Exhibit A of the UCC-1:

STB Transmittal Letter:

Titled Inventory as Collateral (Specific Titled Inventory, Other Specific Inventory and General Inventory):

Titled Inventory as Specific Titled Inventory:

Specific Titled Inventory is a narrow, clearly identified subset of collateral e.g. assets that have certificates of title and each item is individually listed and identified. Property that requires a certificate of title, such as: Motor vehicles, Trailers, Mobile equipment, Vessels, Aircraft.

References in the Security Agreement (Section B) & Exhibit A of the UCC-1:

Titled Inventory as Other Specific Inventory:

References in the Security Agreement (Section B) & Exhibit A of the UCC-1:

Titled Inventory as General Inventory:

References in the Security Agreement (Section B) & Exhibit A of the UCC-1:

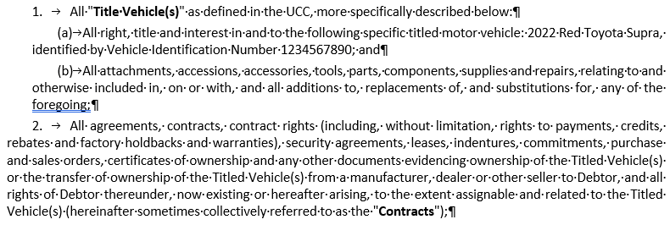

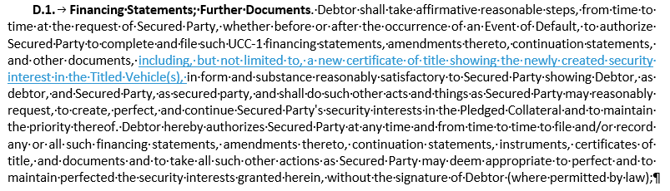

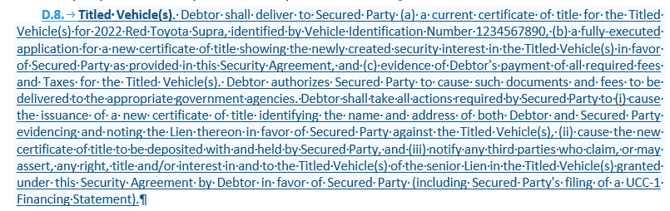

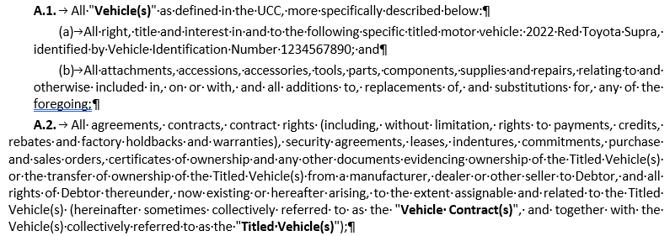

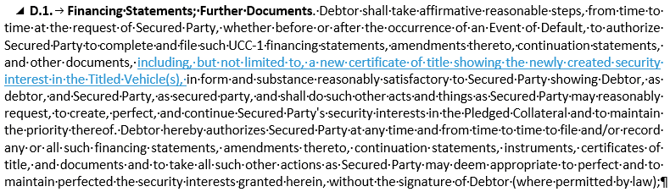

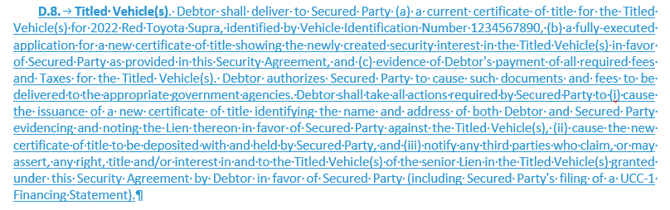

Titled Vehicle as Collateral:

References in the Loan Agreement (Defined Terms, C.4(c),D.9(x)):

![]()

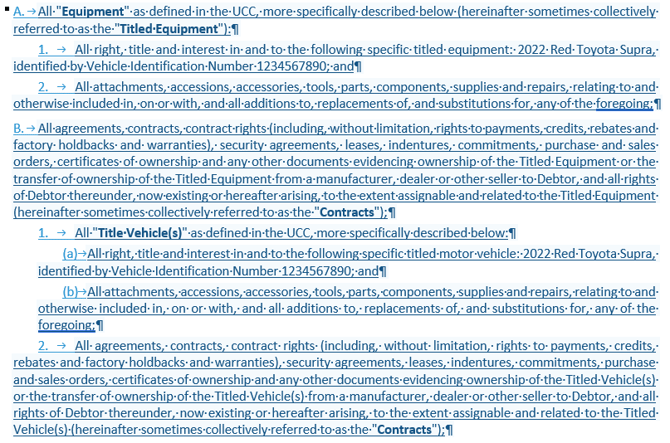

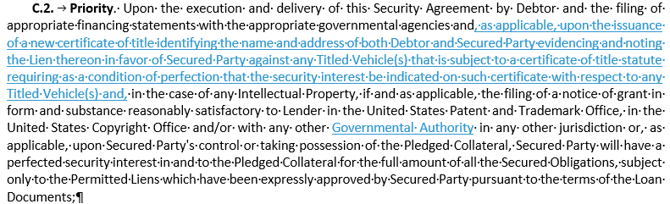

References in the Security Agreement (Section A, C & D):

References in the Exhibit A of the UCC-1: